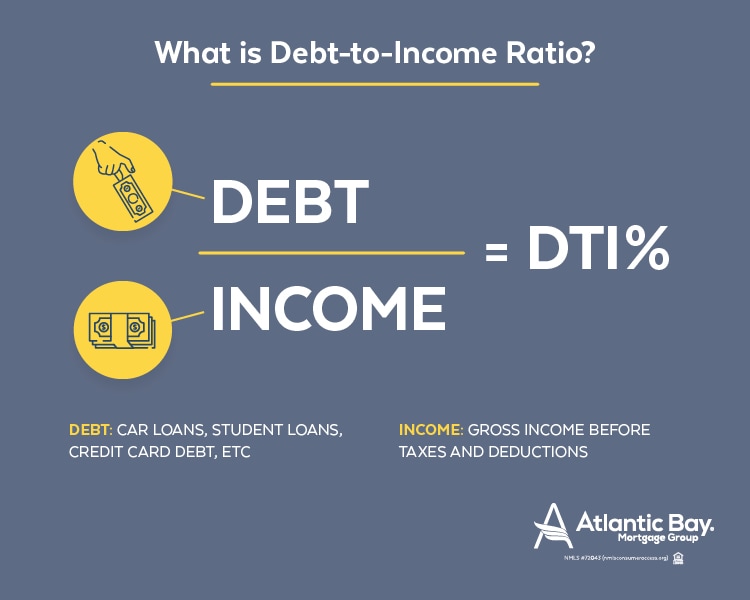

If you find it's too hard, you'll understand you need to change your expectations downward. Mortgage lenders consider not just your credit however also your debt-to-income ratio when you make an application for a loan. This ratio compares total financial obligation payments to your gross regular monthly income. For example, if your gross regular monthly income is $4,000, your home loan will cost $1,000 monthly and all other debts include up to $500, your debt-to-income ratio is $1,500/$ 4,000 or 37.

Normally, your debt-to-income ratio can't go beyond 43% to receive a home mortgage, although numerous lending institutions choose a lower ratio. If you owe a great deal of cash, you're going to have to pay down some of it to get authorized for a loan to purchase a home. Paying down financial obligation likewise assists improve your credit, which allows you to certify for a better home mortgage rate and lower regular monthly payments and interest.

Typically, you'll need: Proof of earnings: This can include income tax return, pay stubs, W2s from companies, and 1099s if you're an independent contractor. You'll require to reveal you have actually had stable income for two years. If your earnings was $50,000 yearly up until recently and simply went up to $100,000, your loan provider may only "count" $50,000 in determining what you can borrow.

Bank and brokerage statements provide proof of properties. You'll need many other files after you in fact find a house, consisting of an appraisal, a study, evidence of insurance, and more. However offering standard monetary documents early is very important so you can be pre-approved for a loan. Pre-approval makes you a more competitive house buyer considering that sellers understand you can in fact qualify for funding.

If you get your monetary life in order initially, buying your home must be an excellent experience that assists enhance your net worth-- rather than a financial mess that originates from getting stuck to an expensive loan that's difficult to pay back.

Worried about getting a home mortgage? You're not alone. Customer research studies have discovered that getting a very first mortgage ranks quite high on the tension scale; it's best up there with going to the dental practitioner or getting pulled over for driving too quick. Fortunately, though, a little home mortgage understanding can go a long way toward lowering your stress and anxiety and helping you to get a better home mortgage.

Home mortgage down payment minimum variety from 0% (for VA house loans and Rural Housing home loans) to 20 percent (for non-government loans without any home mortgage insurance coverage), with plenty of options in Helpful site between. There are 97% home mortgage for borrowers with above-average credit rating (the Standard 97) and there are loans requiring just 3.

Some Known Questions About What Type Of Mortgages Are There.

Additionally, there is the piggyback mortgage for buyers with 10 percent to put down, plus a host of other choices consisting of three percent down programs from Fannie Mae and Freddie Mac, and programs such as HomeReady. You do not need to make a downpayment of 20% to purchase a home. Yes, to qualify for a lot of lending institutions' advertised rates, you need a sizable deposit and excellent credit ratings.

For example, the Federal Housing Administration (FHA) guarantees mortgages for debtors whose credit report vary as low as 500. And, in some cases, the FHA will insure loans for customers with no credit report whatsoever. In addition, Fannie Mae and Freddie Mac, which buy and sell most of home loans in the U.S., allow FICO ratings to 620, as does the Department of Veterans Affairs with its VA loans; and the U.S.

Some home mortgage lenders approve loans with scores under 600. When you purchase residential or commercial property, there are fees which are a part of the transaction. There are More help escrow charges, title insurance coverage costs, lending institution expenses, home appraisal services, house assessments, and more. In general, closing expenses are lower than what they utilized to be, but costs can still build up.

Ask the seller to pay your costs. It should not matter whether you pay $295,000 for a home and pay your own expenses, or provide $300,000 and ask the seller to pay $5,000 of your costs. Or, ask the lending institution to pay your expenses. Many lending institutions will consent to this, but you'll be asked to pay a greater mortgage interest rate.

25%) increase in your rate will cover your costs completely. This is referred to as a zero-closing expense home mortgage loan. Last but not least, you can ask the federal government to pay your expenses. Numerous first-time buyer programs include assist with closing expenses. Some even provide deposit help too. Ask a mortgage officer what kind of work history is required to get authorized for a home loan, and the automatic response will be "two years." That's kinda sorta true, but not completely.

Someone who worked as an unpaid engineering intern, and was later on provided a full-time, salaried position is more likely to get authorized than a candidate whose work history includes full-time bartending, followed by a stint at a more info daycare facility, then by part-time barista work and multi-level marketing. This doesn't suggest that both debtor types will not be authorized, it simply means that you never know until you ask.

Call a lending institution and ask to be pre-approved for a mortgage. You'll learn just how much you qualify to obtain, what it will cost, and if there is anything you can do to obtain more, or to pay less. Pre-approvals can be completed in a few minutes. Almost all U.S.

The Buzz on What Is The Harp Program For Mortgages

The process doesn't have to make you nervous, though the more you understand, the better off you'll be. Get today's live home loan rates now. Your social security number is not required to start, and all quotes feature access to your live home mortgage credit scores.

Deciding to become a homeowner can be difficult for lots of first-time homebuyers. The looming concerns of affordability, where to buy, and job security are all genuine concerns that warrant severe consideration. The truth is that there's never a right time or the ideal scenarios to start this journey, but ultimately, you desire to treat house-hunting and the home loan process as you would other major life occasions.

Here are five essential aspects every newbie homebuyer should consider when getting a home mortgage. In a recent S&P/ Case-Shiller report, house costs rose 5. 2 percent. Even with a steady labor market that supports the rate increase, home costs continue to climb up faster than inflation sparking competitors for less available homes (which of the following statements is true regarding home mortgages?).

Granted, when inventory is low, it does become a sellers' market making it harder for purchasers to complete, but dealing with a skilled-lender who can assist assist in the borrower through the process is vital to getting approval. When acquiring a home, employing a team of professionals is a significant element that might determine the success or demise of your mortgage experience.

Bond encourages that when getting a mortgage, make certain that your taxes are filed and organized. Collect your last month of paystubs and ensure you can quickly access the last two months of your checking account. You must also acquire a letter of work from personnels, and check your credit history to figure out if there are any inconsistencies.